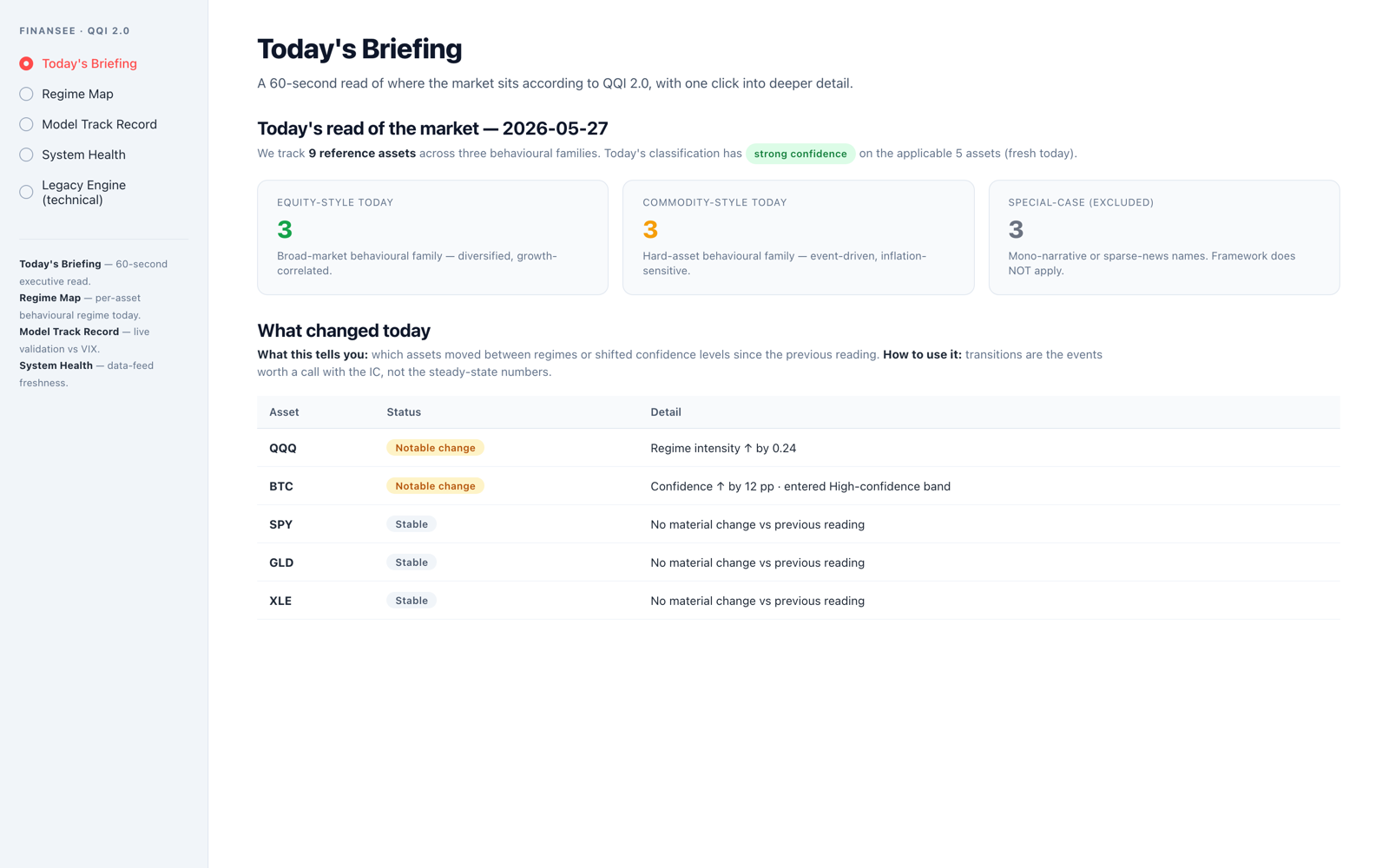

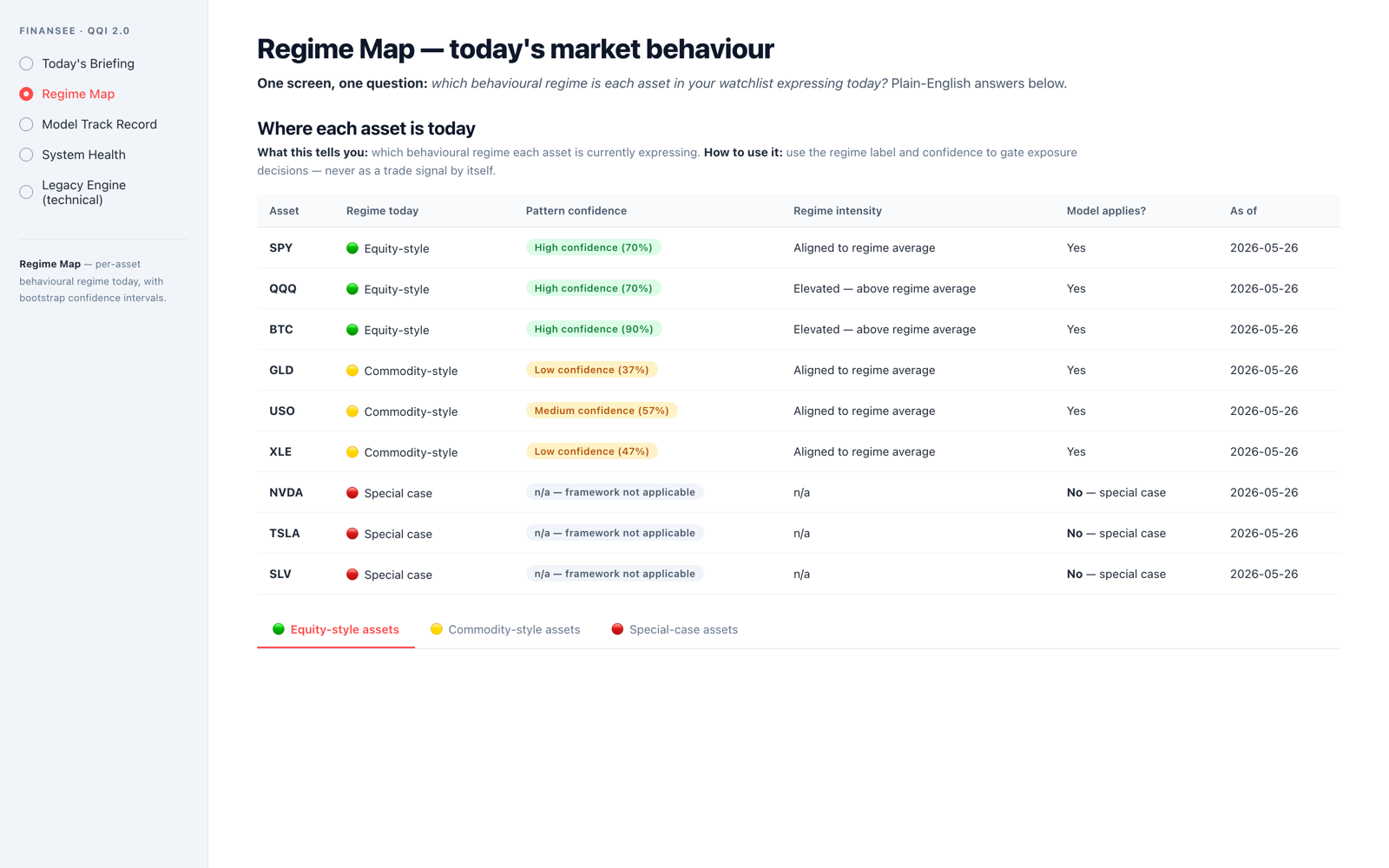

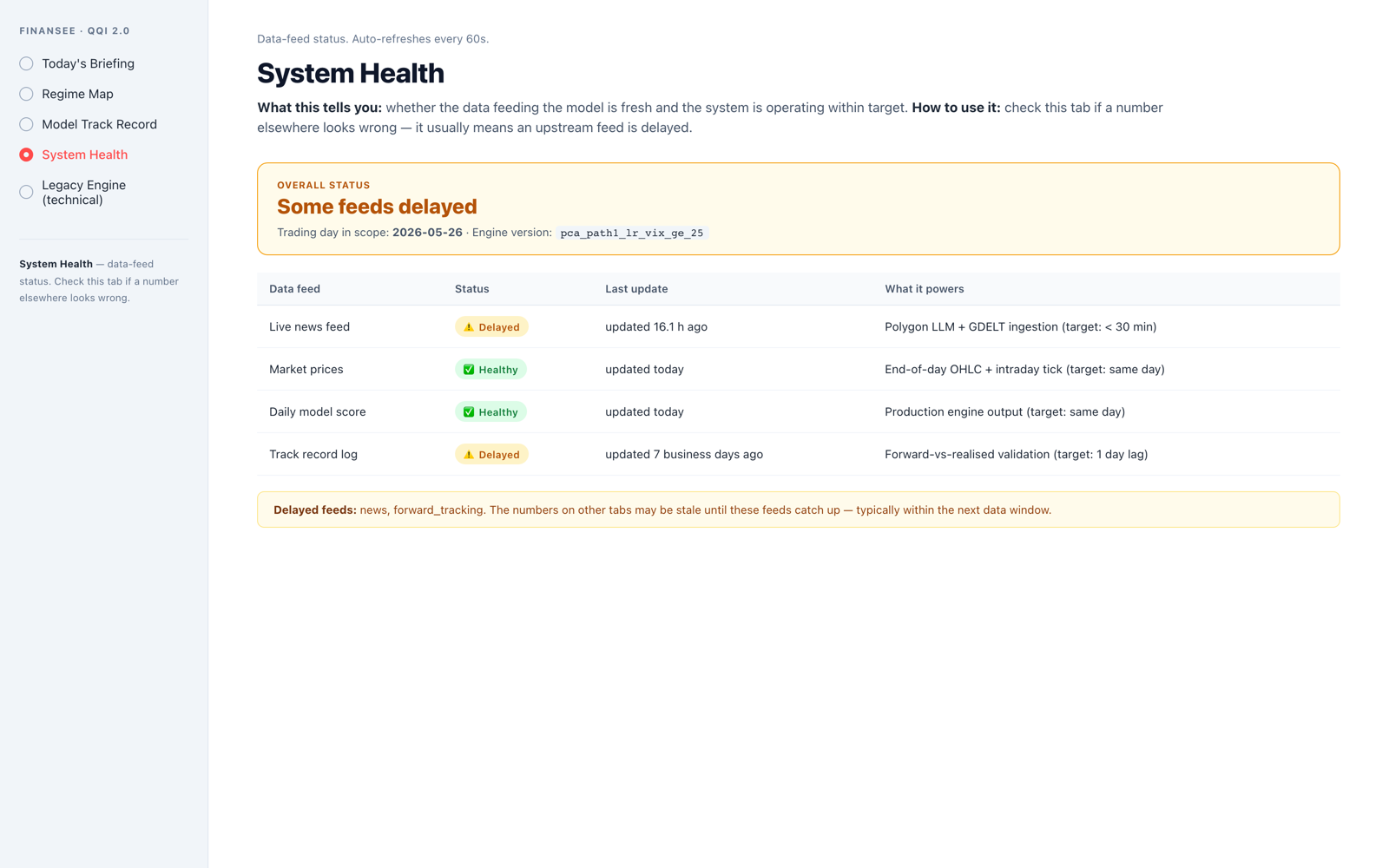

Inside the console

Four views, four jobs to be done — plain English everywhere, technical detail behind expanders for the curious.

Console access is granted to Founding Pilot partners after onboarding. Pilot scope agreed upfront — see the section below.